By Bill Wilson — On Oct. 26, the Bureau of Economic Analysis’ advance estimate of the Gross Domestic Product (GDP) in the 3rd quarter (Q3) of 2012 showed 2 percent growth — not really a good number.

By Bill Wilson — On Oct. 26, the Bureau of Economic Analysis’ advance estimate of the Gross Domestic Product (GDP) in the 3rd quarter (Q3) of 2012 showed 2 percent growth — not really a good number.

Just to get to the 3 percent annual growth rate the Obama Administration had originally forecast at the beginning of the year, the economy would have to grow at an annualized pace of 6.7 percent in the fourth quarter — something not likely to happen.

In fact, the numbers look even worse upon examining the fine print, because 20 percent of the nominal increase in GDP was attributable to increased government spending. If government spending had held steady, as it had the prior two quarters, growth would have only come in at a reported 1.6 percent.

That result prompted a study at Americans for Limited Government into what would happen if one takes government spending out of the equation entirely and then calculates the growth rate of the private sector alone.

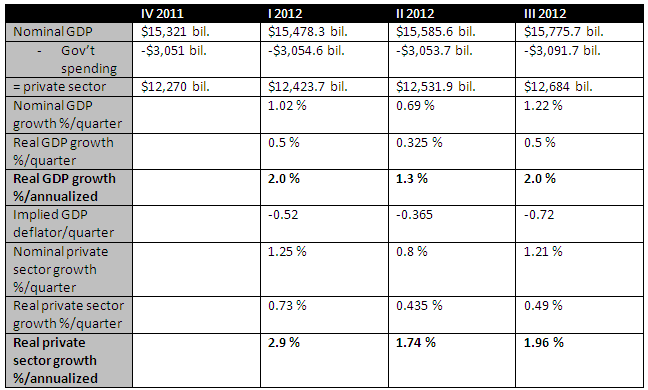

The study shows annualized growth of the GDP versus that of the private sector with government spending removed as a component. So for example in Q1 2012, the GDP grew by 2 percent, but the private sector grew by 2.9 percent. But in Q3, the GDP grew by 2 percent but the private sector only by 1.96 percent. Why?

Because when government spending is included as a component of GDP, and then is held steady or cut, as in Q1, it weighs down the GDP on a nominal basis. And when spending increases, as it did in Q3, it boosts the GDP nominally speaking. This is an inherent bias of the first order in favor of government expenditures when measuring the health of the economy.

The implication of this finding is that one will often not get a good GDP number without dramatically increasing government spending. Moreover, if one physically cuts spending substantially, the Bureau will measure a marked decrease in the GDP. That is, unless the decrease in government spending is offset by an even larger increase of the private sector.

This type of reporting system makes it difficult to chart the effects of governmental policies, particularly expenditures, on the private sector by a mere casual reading of the GDP. It is therefore misleading.

More importantly, it creates a disincentive against legislators ever cutting spending, even if our fiscal house is crumbling, as it is today, because it will cause a technical recession.

Say we had balanced the budget in Q1 2012 with spending cuts. One would distribute the actual $1.2 trillion deficit for the year throughout each of the following four quarters, resulting in $300 billion less in government consumption expenditures and investment in each quarter. This is a rough estimate because oftentimes appropriations stretch out over several years. But, for the sake of simplicity, let’s assume $300 billion less spending per quarter.

Assuming no immediate impact on private consumption, the GDP in Q1 2012 would have come in at $15,178.3 billion, a nominal decrease of $142.7 billion. Converted into real GDP, the economy would have contracted by a reported annualized rate of 4.2 percent.

If one assumes an immediate one-to-one impact on private consumption and investment, the GDP in Q1 2012 would have come in at $14878.3 billion, a nominal decrease of $442.7 billion. Then the reported rate of contraction would rise to 12 percent in terms of real GDP.

What would actually happen is probably somewhere in between a reported 4.2 and 12 percent reduction of GDP immediately.

Suffice to say, there would likely be at least two quarters of negative growth resulting from spending cuts of that magnitude — and that’s probably on the low end, considering what happened after World War II. Then, the economy “contracted” by 1.1 percent in 1945, by a whopping 10.9 percent 1946, and then again in 1947 by 0.9 percent.

But was the economy really contracting? Or was spending simply decreasing?

All of this underscores why government spending should probably not be included as a component of the GDP — it is a misleading indicator of true economic health. But even more so, it emphasizes why we need a real private sector recovery in this economy.

Especially when one considers the composition of our workforce.

Only 22 million Americans work for government at the federal, state, and local level, just 15 percent of the 143 million people who have jobs. Yet close to 23 million Americans cannot find full-time work in this economy, and another 5 million have given up looking.

There will be no recovery from this depression without a robustly growing private sector, because we cannot all work for the government. We need to grow the real economy, and going forward, the public will need useful metrics that do not double-count the impact of government spending on economic output.

Bill Wilson is the President of Americans for Limited Government. You can follow Bill on Twitter at @BillWilsonALG.

{kind=link}