The unemployment rate once again increased to 4.4 percent after decreasing for two consecutive months, as the unemployment level jumped 208,000 to 7.57 million, according to the latest data compiled by the U.S. Bureau of Labor Statistics.

The unemployment rate recently peaked in November 2025 at 4.5 percent, and the unemployment level at 7.78 million. Just another 21,000 unemployed and it would represent a new high in unemployment for this cycle, extending the upward trajectory that began rising in Sept. 2022.

The unemployment level itself had been rising for about 37 months from Sept. 2022 to last November, with the record in modern history being 39 months from a low of unemployment to a high of unemployment from March 1989 to June 1992 when it rose 3.8 million to 10 million.

Meaning if it rises again to a new near-term high in March, it would mark a record amount of time for unemployment to be rising to 41 months from the low to the potential high, but with some idea that it should eventually stop rising. After all, why would the labor market contract for much longer than the longest time ever? We should be nearing peak unemployment or already at it.

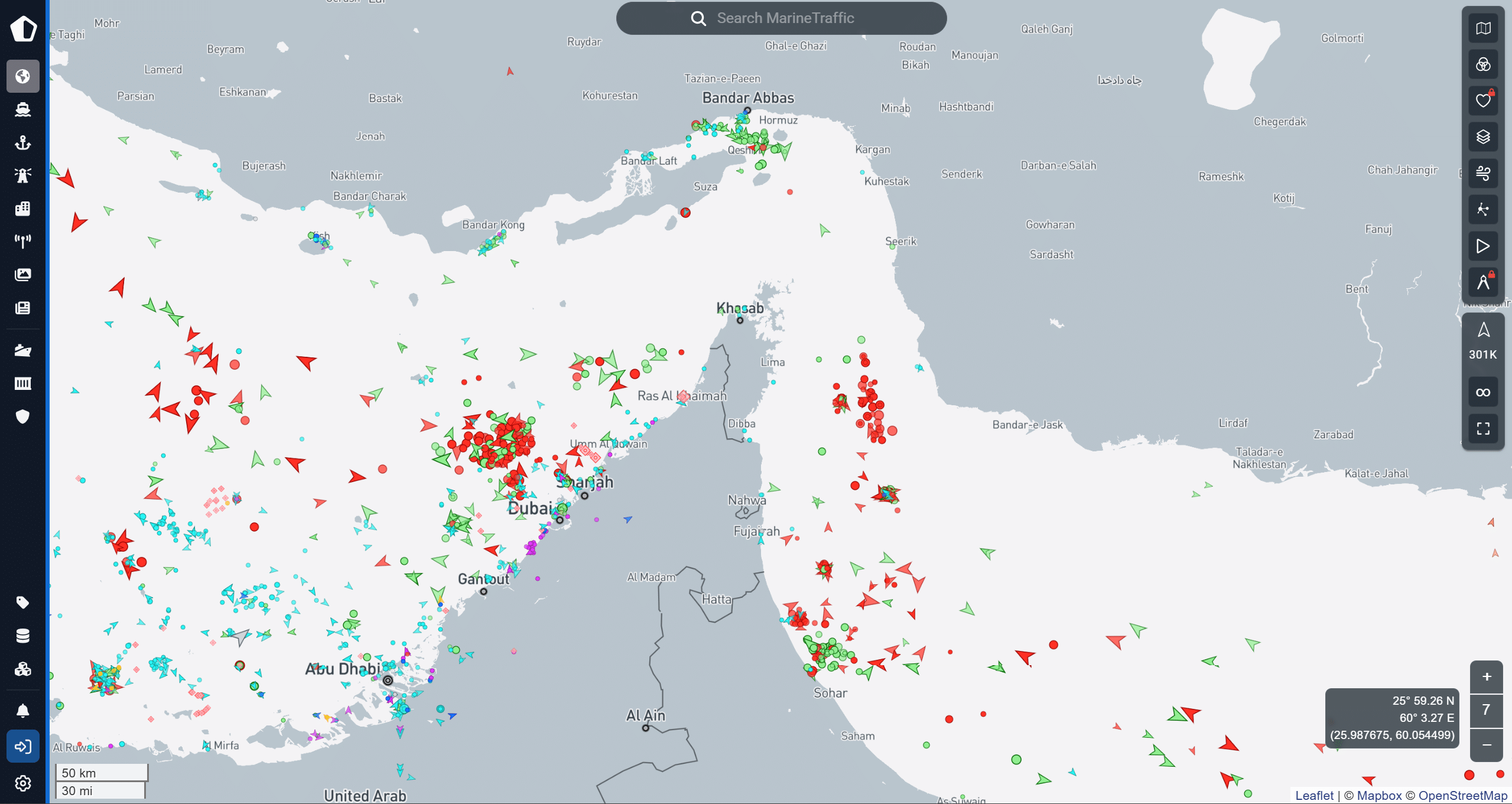

The news comes as oil prices are once again surging amid the U.S. and Israeli war on Iran, with oil and other shipments out of the Persian Gulf that would normally run through the Strait of Hormuz practically ground to a halt at the moment even as President Donald Trump has offered armed U.S. Navy escorts and new war risk insurance for a container ships and oil tankers.

According to Bloomberg News’ Serene Cheong on March 6, reporting on the just two ships going through the Strait of Hormuz in the past 24 hours: “The escalating war in the region has prompted dozens of fully laden oil and gas tankers to stay hunkered down within the Persian Gulf, choking off supplies to key customers in Asia and Europe. The frequency of attacks on ships in and around the strait remains high, making it too risky for energy tankers and their multimillion-dollar cargoes to attempt a transit.”

That’s Iran’s weapon, and they’re going use it, even while their missiles, air force and navy are being rapidly destroyed.

As a result, oil prices are going through the roof, with light sweet crude oil hitting $90 a barrel as of this writing, and Brent crude oil hitting $85 a barrel, up from $55 a barrel and $58 a barrel, respectively, as recently as December 2025.

Meaning, with oil prices up more than 60 percent, so too will this bleed into consumer inflation. Already national gas prices are back above $3 a gallon and rising rapidly amid the global supply crunch.

A similar spike in oil and natural gas prices occurred following Russia’s full-scale invasion of Ukraine in February 2022, contributing to an already inflationary environment following Covid, wherein global production had been brought downward during the lockdowns and in the meantime Congress and Fed were borrowing and printing trillions of dollars. It was too much money, chasing too few goods.

And now it could happen again, with reverberations throughout the economy.

Sometimes, spikes in inflation can precede increases in the unemployment rate, but sometimes, they can go up at the same time, like in 1980 and 2008, when a recession is imminent. Usually a peak in both is felt, and then as unemployment rises, inflation will ultimately cool as demand collapses.

A lot can change in a month, wherein this column had speculated that perhaps the economy was turning a corner, with inflation cooling along with unemployment jumping again. Now, it’s the opposite and the economy is on the verge of hitting a new record in terms of how long unemployment has been rising, dating all the way back to the Biden administration.

The costs be damned, as President Trump is pressing ahead with the war, demanding Iran’s surrender, stating on Truth Social on March 6, “There will be no deal with Iran except UNCONDITIONAL SURRENDER! After that, and the selection of a GREAT & ACCEPTABLE Leader(s), we, and many of our wonderful and very brave allies and partners, will work tirelessly to bring Iran back from the brink of destruction, making it economically bigger, better, and stronger than ever before.”

And, now, that might be the only way to end the pain at the pump. If anyone was wondering why nobody wanted to get too forceful with Iran over the escalating danger of its nuclear weapons program, just look at the price of oil today. It may be a high price to pay today in terms of gasoline, but the price of doing nothing would have been greater.

If you think the oil shock is bad now, just image how bad it would have been had Iran obtained nuclear weapons and was now blackmailing the world.

Robert Romano is the Executive Director of Americans for Limited Government Foundation.