Did anyone notice the Fed inverted the yield curve?

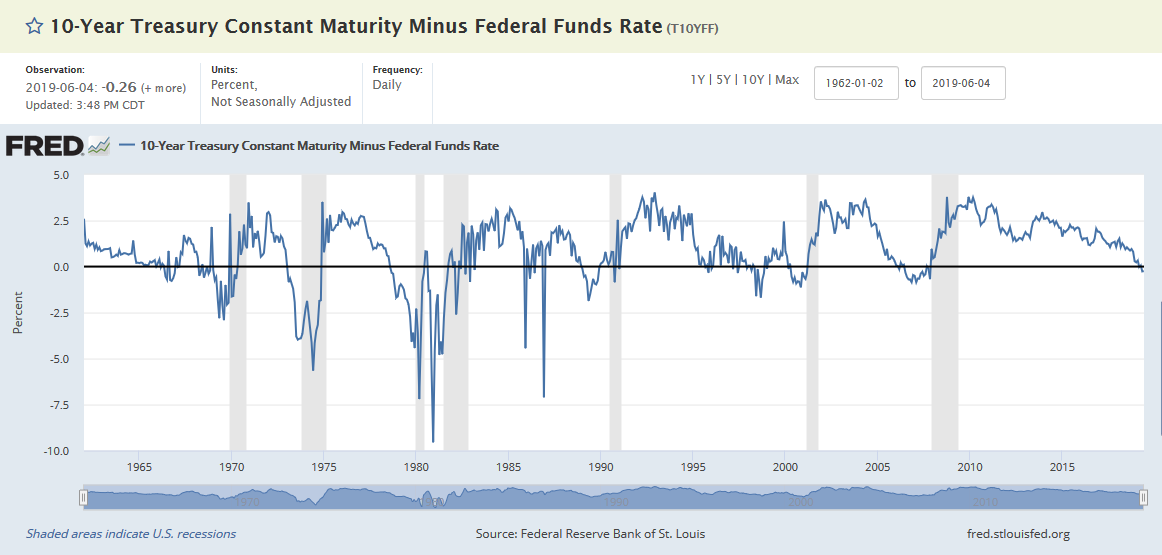

On May 23, the 10-year Treasury dipped below the federal funds rate, the benchmark interest rate set by the Federal Reserve that it currently has set for a range of 2.25 percent to 2.5 percent, and has stayed there since.

As of June 4, the effective federal funds rate was 2.38 percent, while the 10-year is at 2.13 percent. There were also brief inversions on March 28 and May 15, but they immediately came back into positive territory.

Unlike other inverted interest rates, which often foretell a recession in not so distant future, this is one the central bank actually has control over since it sets its own rate. But, there’s no need to panic. The last time those two rates briefly inverted and then stayed inverted, beginning in late March 2006, a recession did not follow until December 2007. It took 21 months.

Sometimes it takes even longer than that. The time before that, the two rates briefly inverted in Sept. 1995, but the next recession did not begin until March 2001, almost six years.

Another brief inversion occurred in Dec. 1985, but the next recession did not begin until July 1990, almost five years.

In the 1970s and in 1980, there were briefer periods of inversion of nine months, 17 months and 10 months, but before that, in March 1966, there was a brief inversion but the recession did not happen for another three years, nine months.

All told, since 1954, the average time it took for a recession after the federal funds rate was 33 months, or nearly three years.

Meaning, the business cycle could be entering its last stage, but it is hard to pin down how long it might take for it to complete. Sometimes it happens fast and other times it’s taken a while. It is useful, therefore, to consider other indicators.

The 10-year, 3-month has inverted, but the 10-year, 2-year has not done so yet. Recessions tend to occur on average about 16 months after the 10-year, 2-year inverts, and so even if it were to invert right now, that might not forecast a recession until Dec. 2020, after the next election.

Also, the unemployment rate still seems to be dropping, currently at 3.6 percent, but once it starts rising, after peak employment has been reached for the first time in a business cycle, a recession comes on average about 11 months later, although in recent history that period has been as long as 16 months. Every time the unemployment rate reaches a new low, that clock gets reset. Tomorrow, on June 6, we’ll get our next read.

In the meantime, as for the federal funds rate, the Federal Reserve tends to follow the 3-month Treasury around, so if the 3-month starts dropping, expect the Fed to cut interest rates. And we should probably assume these will be the final round of rate cuts before the next recession.

On June 4, at the Conference on Monetary Policy Strategy, Tools, and Communication Practices, Federal Reserve Chairman Jerome Powell appeared to be preparing the public for the next downturn. He said, “The next time policy rates hit the lower bound — and there will be a next time — it will not be a surprise.”

Indeed. The fact is, we are along overdue for another recession as it has been almost a decade. So that we might finally be nearing the end of the cycle is not really surprising.

Powell added, “With the economy growing, unemployment low and inflation low and stable, this is the right time to engage the public broadly on these issues.”

That is true. Right now, the numbers look great. The economy grew at 3.2 percent in the first quarter. Unemployment is 3.6 percent, a 49-year low. And inflation is at 2.0 percent. But nothing lasts forever.

The Fed has given itself a little room to begin rate cuts after so many years at near-zero percent. But now the rate is inverted. How long will the Fed wait to leave it like that? Could leaving it inverted for too long cause another recession?

To avoid the appearance of politics, the Fed should hope not.

Another consideration is that since the Fed began dumping bonds back on the market — it has shed $567 billion since Sept. 2017 — short-term interest rates have been steadily rising. This usually happens anyway as the business cycle comes to a close.

Since May, the Fed has gone from dumping $30 billion of treasuries a month to $15 billion, and then in October down to nothing, and then further mortgage bond sales will then be offset by treasuries purchases. This will set the stage for a drop in short-term interest rates and potentially a widening of the 10-year-3-month and 10-year-2-year spreads. This might cure the current inversions. Stay tuned.

If the question is whether we’ll get another recession before Nov. 2020 and the presidential election, it could be close. Recent presidents who lost reelection, Jimmy Carter and George H.W. Bush, each had recessions in 1980 and 1990 respectively to contend with that surely weighed on their chances. In terms of President Donald Trump’s chances, a lot may ride on what the Federal Reserve does next.

Robert Romano is the Vice President of Public Policy at Americans for Limited Government.