“[China is] worried about forever-rising deficits, which may devalue Treasuries by pushing interest rates higher… Inside China there has been a lot of debate about whether they should continue to buy Treasuries.”—JP Morgan economist Frank Gong, “China ‘worried’ about US Treasury holdings.”

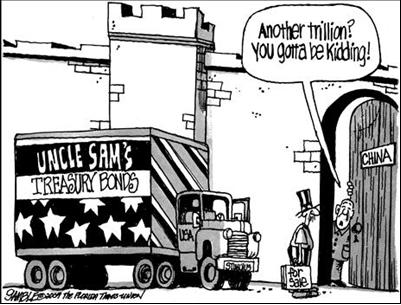

China is worried about the value of nearly half of its $2 trillion in currency reserves that include U.S. Treasury bonds and other notes issued by the U.S. As well they should be.

China is worried about the value of nearly half of its $2 trillion in currency reserves that include U.S. Treasury bonds and other notes issued by the U.S. As well they should be.

They are only as good as America’s promise to pay them back.

And the fact is, both political parties in the U.S. have demonstrated a complete inability and unwillingness to rein in costly federal spending—which with a probable $1.75 trillion deficit should the Obama budget be enacted, makes it less likely that the U.S. ever will be able to make good on that promise.

Congress is already discussing whether or not to push through another “stimulus” (which really means selling more treasuries to China and elsewhere) that would, technically, make it less likely that we can pay back the debts when called in.

It’s a simple principle: The more money one borrows to fuel an out-of-control, unbridled spending spree, the more resources must be dedicated to paying back that debt with interest. If too much debt is incurred, it eventually becomes impossible for the debtor to ever emerge solvent.

And if there was any doubt that the Chinese are indeed worried, one need look no further than recent comments by the Chinese premier, Wen Jiabao, who said, “We have a huge amount of loans to the United States. Of course we are concerned about the safety of our assets. To be honest, I’m a little bit worried… I would like to call on the United States to honor its words, stay a credible nation and ensure the safety of Chinese assets.”

One can almost hear a glass of champagne dropped in the distance. That’s right, turn out the lights, the party’s over.

Only the pixilated salons in Washington’s saloons haven’t gotten the last call from the bartender—that’s the Federal Reserve—just yet. But it’s coming.

Eventually, Congress, the Treasury, and the Fed’s seemingly endless supply of money from overseas will come to a halt. The nation’s creditors can no more afford to continue lending the money on this scale as we can continue to borrowing it. Eventually there comes a tipping point where the debtor is so far underwater, that he or she drowns—and all who would have once thrown a life-preserver are treading water themselves.

At that point, a global run on the dollar would ensue as the debts are called in one after another, leaving the American taxpayer with an insurmountable bill.

At that unthinkable, untenable moment—since there would be no more money left to borrow—something funny would happen. No, the world wouldn’t end. There would certainly be economic turbulence and hardship immediately, but it wouldn’t be the end of civilization. Nor the final chapter of U.S. history.

Very simply, the government would actually have to stop mindlessly spending and pay down the debt until the balance sheet was back to zero.

Really, policymakers are left with two options: wait for the economic Armageddon to come, or prevent it from coming in the first place by paying down the debt now.

And then the Chinese, and other creditors overseas, would need not worry about the worthless pile of paper they are holding in reserve. It will have regained its intrinsic value it once held when first issued. And the American taxpayer will not be burdened with using a wheelbarrow to go grocery shopping. Or a rickshaw.

Robert Romano is the Senior Editor of ALG News Bureau.