By

By Correction: The national debt reached $9 trillion in 2007.

We’ve seen this movie before. And one can only hope that this is the episode where the Creature returns beneath the high seas from whence it came, ne’er to return, sparing the Ship of State from ultimate destruction.

But as Axel Merk recently wrote, “hope is not a strategy.”

During World War II, the Fed “monetized” the national debt—printing money to directly purchase U.S. Treasury debt—beginning in 1942. According to FOX Business, “At the beginning of World War II, the Fed did its part for the war effort, agreeing to peg the Treasury bill rate at 3/8% and the Treasury bond rate at 2 1/2%. That kept down the cost of the massive amounts of money the U.S. had to borrow. The Fed maintained the peg by becoming the default purchaser of Treasury debt, buying enough to keep the rates down.”

By 1947, it owned $15.5 billion out of $16 billion in outstanding treasuries—and inflation behaved predictably. By June the Consumer Price Index had hit 17.6 percent. According to the Fed Chairman, Mariner Eccles, the policy of fixing treasury and bond rates to finance the national debt “[made] the entire banking system, through the action of the Federal Reserve System, an engine of inflation.” By 1951, the Fed would no longer agree to keep the treasuries rate and bond rates pegged, and it reasserted its independence.

Since the war years, the government has still financed the growth of the national debt through the sale of treasuries and other government debt. Indeed, since 1958, the debt has grown every single year, until today as it has reached the catastrophic heights of $11.4 trillion.

Over time, the Fed’s “independence” has eroded in favor of political considerations, as ALG News recently reported in “The Ongoing Presidential Policy of Inflation.” To be certain, the government since 1951 took a “kitchen sink” approach to inflating the currency to fuel government spending under Presidents Truman, Eisenhower, Kennedy, Johnson, and Nixon. By 1971, the American gold standard was abolished. In 1978, the Full Employment Act was adopted, establishing the dual mandate of the Federal Reserve: to perpetuate economic growth and maintain price stability.

It was only when the confluence of subsequent Fed, Congressional, and agency policies came to a head once again that the practice of debt monetization has begun anew. And then, only because the government has not been able to borrow money at a fast enough pace to keep up with the rapidly deteriorating financial system. Overseas, creditors in China, Russia, and elsewhere are slowing their purchases of more treasuries, as ALG News recently reported in “The Gathering Storm Over the Dollar Bears No Quarter.”

Unless the government can roll back out-of-control spending, it is left with two politically unpalatable options to balance the budget: raise taxes, or monetize the debt.

Just yesterday, the New York branch of the Federal Reserve purchased another $7.45 billion in treasuries, this time bonds maturing March 2014 through August 2015. To date, the Fed has bought more than $170 billion worth of treasuries this year alone out of a $300 billion 2009 campaign designed to ease borrowing costs, incentivize lending, and to assist the federal government in financing its $1.85 trillion budget deficit.

This represents the first time the Fed has purchased treasuries since 1951, when the practice was put to an end during the Korean War. Today, the Fed is expected to make an announcement about the practice.

Of course, yesterday’s $7.45 billion purchase comes as a part of the some $12.8 trillion the government has already committed for the financial rescue, as reported by Bloomberg News. Some $7.76 trillion of that is from the Fed alone, including $1.6 trillion for the purchase of Fannie Mae and Freddie Mac debt and mortgage-backed securities.

In comparison, the $300 billion committed to purchase treasuries appears to be a pittance—but it is debt monetization nonetheless. And it will be inflationary.

As if it could not get any worse, the Obama Administration has proposed making the Fed the regulator of systemic risk in the financial system. This, as ALG News has previously reported in “Mr. Crassus, Meet the Federal Reserve,” is a lot like putting an arsonist in charge of the fire department.

The Fed’s complicity in the crash of 2008 cannot be understated. The housing bubble was greatly accommodated by the Federal Reserve, which poured the necessary cash into the banking system through monetary easing and low interest rates throughout the 1990’s and 2000’s. The spigots were on—and the “liquid” flowed into banks on a gargantuan level, much of it into home sales.

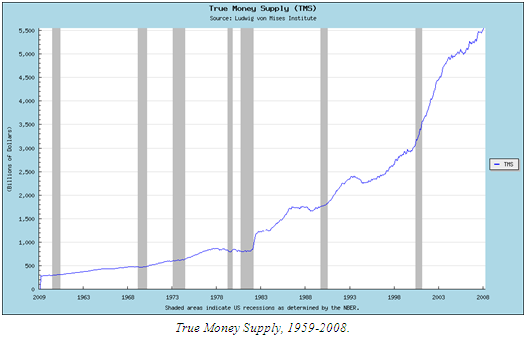

By how much? According to the True Money Supply index from the Ludwig Von Mises Institute, the money supply rose from about $1.787 trillion at the end of 1990 to about $5.268 trillion by the end of 2007, representing a 295 percent increase.For comparative purposes, in that same period, gold rose from $386.20 an ounce to $695.39, a 180 percent increase, oil rose from $23.19 a barrel to $64.20, a 277 percent increase, and the national debt rose from $3.23 trillion to $9 trillion, a 278 percent increase.

As for mortgage debt, its growth dwarfs even that of the actual money supply. In 1990, outstanding mortgage debt held was $3.805 trillion. Suffice to say, by the end of 2007, total mortgage holdings rose to $14.568 trillion, a staggering 383 percent jump.

Throughout that period, mortgages were sold on the secondary market, and the money flowed back into the banks so that more loans could be given. Government Sponsored Enterprises (GSE’s) Fannie Mae and Freddie Mac played a tremendous role in the secondary mortgage market through the securitization of trillions of dollars of mortgage-backed securities (MBS) and related debt—some $4.7 trillion as reported by Bloomberg News by November 2007 rising to over $5 trillion by the time of TARP according to the Wall Street Journal—that were sold all around the world.

Through the sale of securities, more money flowed back into Fannie and Freddie to purchase more mortgages from loan originators. Of note, China was the single largest purchaser of paper from Fannie and Freddie. They held some $500 billion worth by some estimates last summer—just as the mortgage giants were being nationalized, according to the Wall Street Journal.

This system could not perpetuate itself, and yet it was designed as if it would. Two critical government failures occurred at the outset and were compounded over time. The first, from the Fed to keep interest rates low; and the second from GSE’s Fannie and Freddie to guarantee virtually every mortgage in the country.

These had two impacts that were like steroids for the housing market. The former incentivized borrowing, since the rates were low, and the latter incentivized lending, since loan originators could give loans and rapidly sell them off at a profit as housing prices soared. It was a bubble, obviously, and it was one that would have been impossible without these errant government policies, namely those of the Federal Reserve, Fannie Mae, and Freddie Mac.

And now that the bubble has come crashing down, in order to prevent such a calamity from happening again, the American people are told, they must give more power to the Federal Reserve—to the Creature—to fully regulate the financial system.

The truth needs to be told. The Fed cannot save this system, because it possesses neither the capability nor the will to rein in the true systemic risk to the American economy: the unsustainable debts and obligations the American people are being saddled with by the government that pretends to represent them. Between the $12.8 trillion in bailouts, the $11.4 trillion national debt, and the $104 trillion in unfunded Medicare and Social Security liabilities, American taxpayers are on the hook for some $128.2 trillion, or 899 percent of GDP $14.264 trillion.

Put simply, there is no way the Fed can print enough money to help the government to meet its obligations. It couldn’t in 1951, and it cannot now, no matter how much power Congress is asked to bestow upon it. It’s simply impossible. And it is the wrong prescription to pretend that these boom-and-bust cycles can be “regulated” with any precision when it has never worked.

Which is one reason of many why the Obama Administration’s financial proposals at FinancialStability.gov—which reward with more powers those most responsible for the nation’s monetary miasma—should be rejected outright. Before the creditworthiness of the nation is downgraded, the people completely bankrupted, and the global monetary system collapses.

Because the American people do have a choice. This is supposedly a representative government. And the representative branches of Congress can express the will of the people and reject the theft of an entire generation’s wealth—before they ever earn it. Instead of being promoted, the Fed should be audited. The American people have a right to know how the Fed intends to allocate what remains of the nation’s wealth.

After all, this movie does not have to end unhappily. Instead, the Creature can be sent back beneath the high waves, and the Ship of State saved. But the nation’s representatives will have to make some politically courageous decisions: to eliminate the federal subsidization of mortgage, student, and consumer debt, to radically reduce the federal budget, and to pay off the national debt.

Robert Romano is the Senior Editor of ALG News Bureau.