- On: 02/16/2010 09:29:05

- In: Fiscal Responsibility

- By Robert Romano

“[A] foolish man devours all he has.”—Proverbs, 21:20.

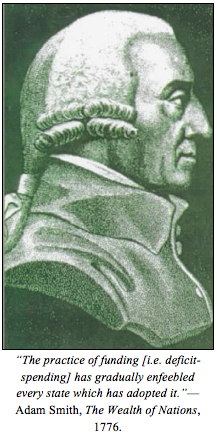

In 1776, when Adam Smith published The Wealth of Nations, Great Britain was faced with a monumental sovereign debt crisis that would not be seen again until the 21st Century — when the U.S. finds itself with a rapidly accelerating $12.4 trillion national debt, soon rising to 100 percent of the Gross Domestic Product within a few years. The last chapter of his opus magnum, “Of Public Debts,” was dedicated to persuading the British Parliament of the calamity the British Empire was faced with. And, alas, they did not listen.

Reading through it today, one might easily surmise that Adam Smith, the Scottish economist and Enlightenment political philosopher, was actually a time-traveler who had foreknowledge of the crisis that faces the world today. For, the crisis he describes in exquisite, haunting detail is, nearly verbatim, eerily reminiscent of the calamity that now threatens the economic survival of the modern world — and threatens to enslave future generations for decades to come.

But, the truth is, there is nothing new under the sun. The crisis today that the U.S. faces — and troubled European debtor-nations Greece, Spain, Portugal, and Italy — with the increasing risk of a national debt default, is just the latest example in the factual and unfortunately oft-repeated economic history of the world. And Smith saw it coming.

In short, republics, empires, and other nations since the dawn of time have fallen for the same exact reason: they spent far beyond their means.

Smith, an inexhaustible student of economic history, cited numerous examples in history back to ancient Rome of nations that had ruined themselves from within by violating the critical principle of parsimony: “ordinary expense [ought to be] equal to… ordinary revenue, and it is well if it does not frequently exceed it.” As early as 1776, Smith was advocating for a balanced budget, a lesson that, tragically, has gone unheeded in the halls of Congress.

“The practice of funding [i.e. deficit-spending] has gradually enfeebled every state which has adopted it,” he noted, citing the decline of the Italian city-state republics Genoa and Venice that “seem to have begun” the practice, Spain with its high taxation and insurmountable debt, the example of France in spite of its considerable natural resources, and the Dutch Republic, that too was overburdened by public expenses and debts that could not be paid.

Smith further warned that Great Britain was not immune: “Is it likely that in Great Britain alone a practice, which has brought either weakness or desolation into every country, should prove altogether innocent?” Indeed. Unfortunately, Treasury Secretary Timothy Geithner has apparently not read his Smith recently, hence his misguided prophesy that the U.S. “will never” lose its Triple-A rating.

Witness today, where the expansion of debt in 2010 at $1.556 trillion will exceed 10 percent of the Gross Domestic Product, far in excess of Barack Obama’s projected, much-hoped-for rate of economic growth for 2010 of 3.6 percent. In fact, the growth of the debt will average $1.06 trillion every year until 2020, under Obama’s ten-year plan, again in excess of the liberal $955 billion average, annual growth the White House projects.

Smith, it turns out, was right. The extension of the public debt by his nation was unsustainable. And Great Britain’s vast empire did, indeed, fall as it repeatedly inflated its currency to pay off the debt, until finally, the Great Depression forced it off the gold standard, never to return to its former preeminence in world affairs.

Smith noted the root causes of such recklessness: “The government of such a state [with the ability of the private sector to lend to the government for a profitable return] is very apt to repose [i.e. rest] itself upon this ability and willingness of its subjects to lend it their money on extraordinary circumstances. It foresees the facility of borrowing, and therefore, dispenses itself from the duty of saving.”

That, of course, is exactly what the U.S. has done. As the nation took on superpower status after World War II, the national debt has grown for every single year since 1958 through the sale of Treasuries and other securities.

Contrast this with how Smith defined a creditor nation, which “derives a considerable revenue by lending a part of its treasure to foreign states… by placing it in the public funds of the different indebted nations… The security of this revenue must depend, first, upon the security of the funds in which it is placed, or upon the good faith of the government which has management of them; and secondly, upon the certainty or probability of the continuance of peace with the debtor nation. In the case of war, the very first act of hostility, on the part of the debtor nation, might be the forfeiture of the funds of its creditor.”

One can only be a net creditor if revenues exceed outlays, thereby saving for a rainy day. If a nation saves nothing, then it must contract debt in times of war and other extraordinary circumstances: “The want of parsimony in times of peace, imposes the necessity of contracting debt in times of war. When war comes, there is no money in the treasury but what is necessary for carrying on the ordinary expence of peace establishment.” Smith strictly warned against violating parsimony during peace, saying it was foolish to “spend upon… pleasures so great a part of [the nation’s] revenue as to debilitate very much the defensive power of the state.”

Yet, that is exactly what we have done. Soon, U.S. defensive capabilities will indeed be undermined if U.S. debt is downgraded, as the costs of outfitting our vast, volunteer armed forces would necessarily skyrocket. Such a development would be severely destabilizing, with aggressor nations seeking to supplant the fallen U.S. giant as it withdraws from the world stage. In this sense, the ballooning debt is a threat to national security.

There is no question that the U.S. has begun to far exceed even the basic limitations outlined by Smith, creating what the economist termed “perpetual debt.” Something’s got to give, as the current state of affairs cannot long endure. Moody’s has warned the U.S. against the Obama ten-year budget plan, which will add some $10.634 trillion to the national debt by 2020. According to the warning, “If the current upward trend in government debt were to continue and become irreversible, the [nation’s Triple-A debt] rating could come under downward pressure.”

Now, the U.S. faces an intractable situation. Net interest owed on the national debt will grow from the annual $188 billion in 2010 to over $840 billion in 2020. And, that’s assuming the debt rating is not downgraded. As interest rates rise, so too will the risks of sovereign default, leading to a situation where the ability of individuals to lend money to the government will be diminished, as Smith warned, “from a distrust of the justice of government, from a fear that if it was known that they had a hoard, and where that hoard was to be found, they would quickly be plundered.”

Hence, off-shore investment is already increasing, as are savings by individuals, coupled with less domestic investment as the stock market struggles. “In such a state of things,” Smith explained, “few people would be able, and no body would be willing, to lend money to government on extraordinary exigencies.” If the debt is downgraded, the ability to sell Treasuries would be severely undermined.

Critically, Smith foresaw the great debt crisis which we today face: “The progress of the enormous debts which at present oppress, and will in the long-run probably ruin, all the great nations… has been pretty much uniform. Nations, like private men, have generally begun to borrow upon what may be called personal credit, without assigning or mortgaging any particular fund for the payment of the debt; and when this resource has failed them, they have gone on to borrow assignments or mortgages of particular funds.”

That is exactly what has been done today — where $4.331 trillion of the Social Security Trust fund and other government accounts has been borrowed from as of the end of Fiscal Year 2009 to finance annual government expenditures, and Obama has promised to borrow another $2.873 trillion by 2020.

And, as for those who chirpily claim that the debt is only “owed to ourselves,” Smith was rightly indignant: Were “the whole debt [owed] to the inhabitants of the country, it would not upon that account be less pernicious.” Indeed, it is still money appropriated from the private sector and necessarily misallocated, when it would otherwise have been spent investing in new business ventures, and importantly, jobs.

Perpetual debt, thus, expands and perpetuates the useless paper trade of debts, securities, derivatives, and other obligations. These trades today number in the tens of trillions of dollars. Imagine if, instead of purchasing debt, that money was actually invested in real jobs and economic growth.

Smith did offer the means of salvation. But, he was highly cynical that the tough decisions could be made: “When national debts have once been accumulated to a certain degree, there is scarce, I believe, a single instance of their having been fairly and completely paid.” He offered two options out of the mess: inflate the currency, or pay down the debt.

Unfortunately, Smith noted, nations frequently opt for inflation: “The liberation of the public revenue, if it has ever been brought about at all, has always been brought about by a bankruptcy; sometimes by an avowed one, but always by a real one, though frequently by a pretended payment,” that “pretended” payment whereby the government increases the money supply to enable repayment of the debt while simultaneously perpetuating its extension and destroying the purchasing power of individuals.

Specifically, Smith wrote, “The raising of the denomination of the coin has been the most usual expedient by which a real public bankruptcy has been disguised under the appearance of a pretended payment,” and commented with contempt upon its practice: “The honour of a state is surely very poorly provided for, when, in order to cover the disgrace of a real bankruptcy, it has recourse to a juggling trick of this kind, so easily seen through, and at the same time so extremely pernicious.”

Once again, that is exactly what has happened in America. Since 2007 when the crisis began, the Federal Reserve has more than doubled the supply of dollars, beating down the dollar and laying the seeds for eventual hyperinflation.

Smith emphasized the hazards, and specifically predicted the calamity of the 2008-09 bailouts: “A pretended payment of this kind… instead of alleviating, aggravates in most cases the loss of the creditors to the public; and without any advantage to the public, extends the calamity to a great number of innocent people. It occasions a general and most pernicious subversion of the fortunes of private people; enriching in most cases the idle and profuse debtor at the expence of the industrious and frugal creditor, and transporting a great part of the national capital [i.e. money] from the hands which were likely to increase and improve it, to those which are likely to dissipate and destroy it.”

And that is exactly what happened in 2008-09, where delinquent homeowners were repeatedly “rescued” from foreclosure; GM and Chrysler’s bondholders were raped by the UAW; and AIG, Fannie Mae, Freddie Mac, Bear Stearns, Goldman Sachs and others were all bailed out by the Federal Reserve, Treasury and Congress.

Smith cited numerous examples of inflation, either through adulteration by mixing alloy into the coin or by raising its denomination, utilized throughout history to balance the budgets of declining nations, including ancient Rome at the end of the first Punic War, King John of France, Henry VIII, Edward VI, and the minority of Scottish lord James VI. Smith noted the ensuing fury of the public that tends to result, and even cases where “after the greatest adulterations it has almost always been brought back to its former fineness. It has scarce ever happened that the fury and indignation of the people could otherwise be appeased.”

Fortunately, however, the brutish end Smith predicted is not a fait accompli. The American people actually have a choice. According to Smith, debt on the scale the U.S. has incurred, will never be paid “without either some very considerable augmentation of the public revenue, or some equally considerable reduction of the public expence.”

Smith concluded by noting the various means that revenues could be raised, including levying new taxes on the colonies — we saw how that turned out — but ceded that they may be “impracticable,” and Smith suggested that “Any new taxes imposed are rarely sufficient to do more than pay the new interest.”

Therefore, per Smith, “the only resource which can remain… is diminution of… expence.”

In the end, Smith was incensed at attempting to sustain the unsustainable: “[I]f [the nation] cannot raise its revenue in proportion to its expence, it ought, at least, to accommodate its expence to its revenue” and “If the project cannot be completed, it ought to be given up.” In this case, the projects to be given up on are the runaway costs of entitlements spending, which will grow from $1.441 trillion today to $2.641 trillion in 2020, an 83.27 percent increase, overtaking vaster portions of the nation’s budget, which will in comparison grow at a 53.53 percent rate.

By 2020, entitlements will account for 56 percent of all revenue, assuming Obama’s generous 4.97 percent average projected growth each year until then. Add in interest, ObamaCare, and other “mandatory” programs, and “[i]t all will gobble up 80 percent of all federal revenues by 2020, government economists project,” reports the AP.

But, it need not be this way; the principle of parsimony may yet be applied. The debt could be retired within a limited number of years, believe it or not, as Smith suggested, through anticipation: the “assignment or mortgage for a short period of time only… [that] was supposed sufficient to pay, within the limited time, both principal and interest of the money borrowed… Had money never been raised but by anticipation, the course of a few years would have liberated the public revenue, without any other attention of government besides that of not overloading the fund by charging it with more debt than it could pay within the limited term, and of not anticipating a second time before the expiration of the first anticipation.”

At a rate starting at $500 billion a year, for example, the national debt could be paid off in a period of about 30 years. But, it would require great sacrifices to be made by members of Congress, chiefly by cutting favored programs, abolishing entire departments and agencies, and reforming entitlements while maintaining vital defense and security obligations so as to not endanger peace among nations.

In truth, such reforms are the only way for the nation to retain its economic superpower status that was lost by Rome, Britain, and so many others, and to remain the leader of the free world. The alternative of inflating the debt away will surely lead to decline, desolation, wars, and despair, as it always has.

There is another way. If, through the extension of the national debt, our Founders would have envisioned a system whereby one generation could indebt another to pay, with interest, for the opulence of the present, surely they would have limited its extension.

For Americans to insist upon luxuries today that will only result in scarcity tomorrow — and to only permit their indulgence upon the promise that their own children will one day be forced to pay for it — is a moral injustice as hideous as the bonds of slavery themselves.

Robert Romano is the ALG Senior News Editor.