Slower growth, flattening wages, bottoming interest rates, lower inflation expectations, less borrowing, and slowing job creation have all become staples of Allianz chief economic adviser Mohamed El-Erian’s oft-quoted “new normal.”

El-Erian’s “new normal” hypothesis in 2009, when he was still with Pimco, anticipated “coming out of the financial crisis, the economy would not recover in a normal cyclical fashion,” and that “some of the recent abrupt changes to markets, households, institutions, and government policies are unlikely to be reversed in the next few years.”

Instead, “Global growth will be subdued for a while and unemployment high; a heavy hand of government will be evident in several sectors; the core of the global system will be less cohesive and, with the magnet of the Anglo-Saxon model in retreat, finance will no longer be accorded a preeminent role in post-industrial economies.”

But what if the “new normal” is actually nothing new, and instead is the continuation of a downward trend that began more than 30 years ago? Nominal growth, median income, interest rates, inflation, credit allocation, and even job creation have all been trending downward for more than a generation.

And, what if it could all be reducible to a single variable — that is, the growth rate of the working age population?

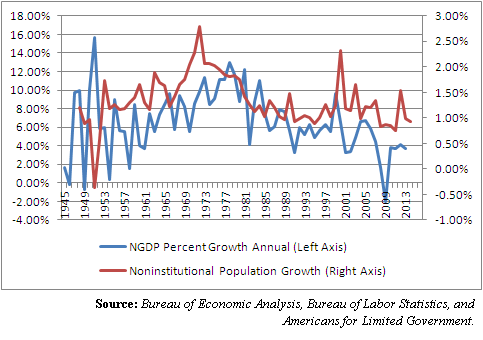

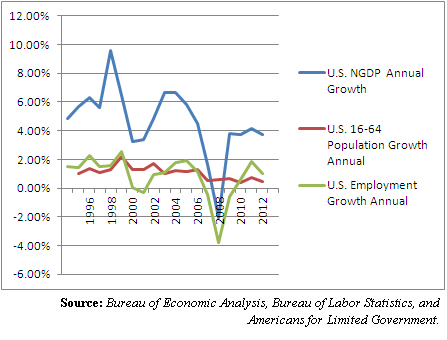

It is hard to conclude otherwise after considering a new Americans for Limited Government analysis of Bureau of Economic Analysis and Bureau of Labor Statistics data of the strong correlation between nominal economic growth and the growth of the civilian non-institutional population aged 16 and older.

The relationship is simple to understand, and based on laws of supply and demand. The faster the working age population grows, the more demand there will be, and the greater the consumption that will occur, all resulting in higher measured economic growth. And, as population growth slows, so too will demand soften, and less consumption will occur, resulting in lower measured growth.

In short, growth is lackluster because demand is low, thanks to slower population growth.

Interestingly, the relationship does not hold up when children are included. Apparently, until individuals reach working age, they are not contributing to additional growth and cannot access credit markets — because they are not producing anything, and hence the 16-year lag.

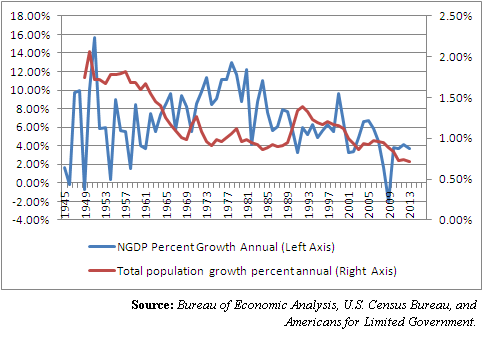

But the real problem with the longer-term growth of the total population is that it has been slowing since 1992, when it most recently peaked at 1.4 percent growth annual. Since then, it has been trending ominously downward — forecasting even slower economic growth in the future.

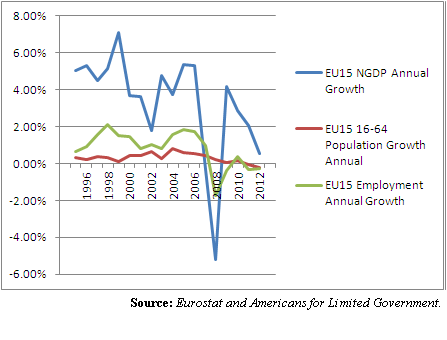

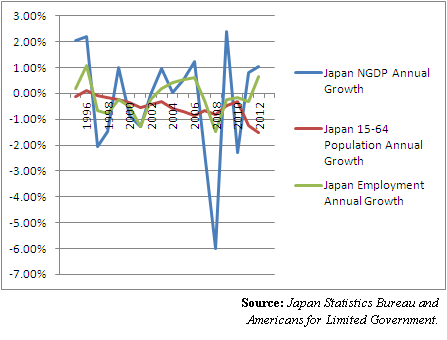

Similar trends can be spotted in Europe, where the working age population growth is even slower than here, and in Japan, where it is contracting.

Looking at data as far back as 1995 compiled by Eurostat and the Statistics Bureau of Japan, it appears all over the developed world, the slower the population grows, the worse the economy performs and the fewer jobs that are created. The U.S. follows a similar pattern over that period.

The idea itself is nothing new. David E. Bloom, David Canning, and Jaypee Sevilla of the Harvard School of Public Health. Department of Global Health and Population have been researching the topic for years, with several studies published by the National Bureau of Economic Research.

In 2001, Bloom, Canning, and Sevilla concluded in a study that, “if most of a nation’s population falls within the working ages, the added productivity of this group can produce a ‘demographic dividend’ of economic growth, assuming that policies to take advantage of this are in place. In fact, the combined effect of this large working-age population and health, family, labor, financial, and human capital policies can create virtuous cycles of wealth creation. And if a large proportion of a nation’s population consists of the elderly, the effects can be similar to those of a very young population. A large share of resources is needed by a relatively less productive segment of the population, which likewise can inhibit economic growth.”

So what does all this mean?

Demographics matter. Aging populations and low fertility do not lead to prosperity. Some argue those trends might be offset with immigration, but if it only includes low-skilled workers, might be counter-productive to the health of the economy.

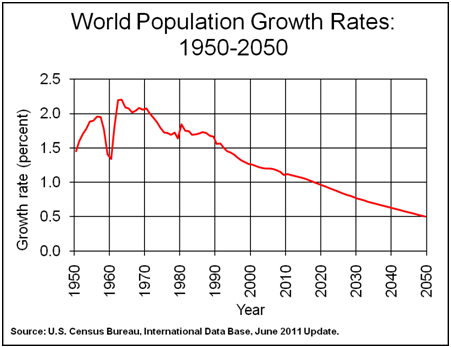

Besides, immigration may not be a long-term solution as slower population growth is expected worldwide over the coming decades. Consider the following chart from the U.S. Census Bureau’s International Data Base, which projects that the global population will continue flattening for the next 35 years, until it will stop growing altogether.

So what to do?

If the model holds up, the only solution to our longer term challenges may be through sustained population growth. Americans and everyone else need to start having more kids, establishing new businesses, and creating new jobs.

Otherwise, we may have to figure how to make do with less demand and thus growth in the future.

Robert Romano is the senior editor of Americans for Limited Government.