“We do not get to add 16 years of deficits and then add that to one year of Gross Domestic Product (GDP), which is what is being done there. If we close the trade deficit then ceteris paribus … we might be able to add one year’s trade deficit back into GDP. That $500 billion, making current year GDP $18.7 trillion, not the $27 trillion stated.”

That was Forbes.com contributor Tim Worstall disputing a piece by this author, “China and the world’s trade war against the U.S. — and why we’re losing,” where I wrote that if “$8.7 trillion [of trade deficits since 2000] had never been shifted overseas, the Gross Domestic Product (GDP) would be nearly $27 trillion today.”

Let’s assume for a moment that Worstall is correct, and that the only thing that would have happened if the trade deficit had been balanced in 2000, all other things being equal, was you’d be looking at a stimulus of only $500 billion above today’s current dollar $18.2 trillion GDP, and not $8.7 trillion, the actual number for trade deficits since 2000.

To have balanced that deficit would have been no easy task. It would have required dramatically increasing domestic production of crude oil, manufacturing more products here in the U.S. by investing in the factories of the future and foreign countries suddenly stopping the devaluation of their currencies with the aim of boosting their own exports. This in turn would have helped boost U.S. exports and reduced U.S. demand for certain imports.

In short, hell would have had to freeze over.

But let’s say charitably we had gotten all those things by 2000, when the GDP was $10.3 trillion. Could it have achieved a $27 trillion GDP? To get there would have required robust growth of a little more than 6 percent nominally a year. So I say, yes, it was very much doable.

Without reservation.

Primarily, because from 1945 to 2000, the U.S. actually averaged 7.18 percent nominal growth a year with just an average annual trade deficit of about $50 billion, according to data compiled by the Bureau of Economic Analysis and the U.S. Census Bureau. Comparatively, after 2000 — the same year Congress granted permanent normal trade relations with China — our average annual nominal growth rate has only been 3.8 percent with average trade deficits of more than $500 billion.

To say we could not have accomplished 6 percent nominal growth annually with no trade deficit when we killed that number throughout the entire postwar dataset fails to recognize the compounding nature of economic growth. To say nothing of any additional inflation that might have occurred, which would have technically also added to nominal economic growth as well.

All we needed was an extra 2.2 percent of nominal growth each year. Guess what the trade deficit was in 2000? $372 billion, constituting 3.6 percent of the then $10.3 trillion economy. Don’t think balancing that deficit would have had a compound growth effect on the economy? Think again.

If anything, a $27 trillion economy might have been conservative estimate, since, given the above premises — energy independence, factories of the future to offset lower labor costs overseas and no currency manipulation — it is conceivable the U.S. economy would have become a net exporter almost overnight, with trillions of dollars of trade surpluses over those same 16 years instead of the $8.7 trillion of deficits we experienced.

The point was to consider what if the same growth we helped create overseas in emerging markets by running the $8.7 trillion of trade deficits since 2000 had occurred here instead. If it had, the economy would be much larger and it would have created millions of jobs. And whatever did not flow to job creation might have been put into new companies or infrastructure or health and retirement systems or upgrading our missile defense or expanding into space economization or all of the above.

Having the $8.7 trillion of trade deficits “all invested back into the U.S. economy,” in Worstall’s words, into U.S. government treasuries, mortgage-backed securities, corporate debt or equities, which are then owned by foreign governments and investors is not the same as the alternative. Which is, profits in companies earned by Americans offering jobs to Americans, rising incomes and additional demand for labor.

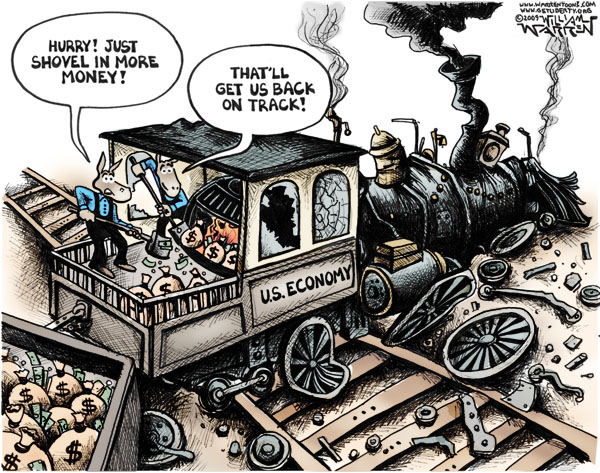

Having the rest of the world buy U.S. dollar-denominated assets may help boost asset prices and debt here — that is to say, they create asset bubbles — but they do not add to growth per se. If that’s the best we can offer, is it any wonder more and more Americans are calling our trade policies into question? In the meantime, the $8.7 trillion of trade deficits unquestionably boosted production overseas, increasing foreign economic growth. Somehow they gained trillions of dollars of GDP but we didn’t lose any. Yeah right.

To be fair, Worstall acknowledged that balancing the trade deficit might have increased investment in the U.S. after all: “Well, yes, OK, we can see that point. If we’d not been spending all our cash on Chinese [trinkets] then maybe the money would have been invested in interesting companies, by government into infrastructure and so on. It’s certainly possible that this would have happened.”

Certainly possible, indeed. It’s the whole reason I wrote the piece.

Particularly, it would have been possible to increase investment here, I would add, if we had been running surpluses instead of deficits, which itself is not beyond the realm of possibility considering the stimulative effect of increasing production here. Instead the U.S. is acting like a majority shareholder of a company that no longer generates any revenue on a net basis and in the meantime offsets the losses by borrowing money and selling more shares, all the while pretending he or she is coming out ahead.

We can get away with it — for now — because we can rely on the Federal Reserve’s printing press and the dollar’s reserve currency status. But how long do we suppose that will last? All we’re doing is making the dollar overvalued as a medium of exchange, shipping production overseas and hollowing out our economy, in the process losing potential growth to the tune of trillions of dollars.

At some point, the world will view the U.S. as adding little to no value, and when that happens, watch out.

In the meantime, to suggest that the U.S. economy could not have grown at a nominal 6 percent or better after 2000 with no trade deficit to get to a $27 trillion GDP — when we nominally grew above 7 percent from 1945 to 2000 with far smaller trade deficits and only at 3.8 percent from 2001-2015 with $8.7 trillion of trade deficits — is preposterous.

Robert Romano is the senior editor of Americans for Limited Government.