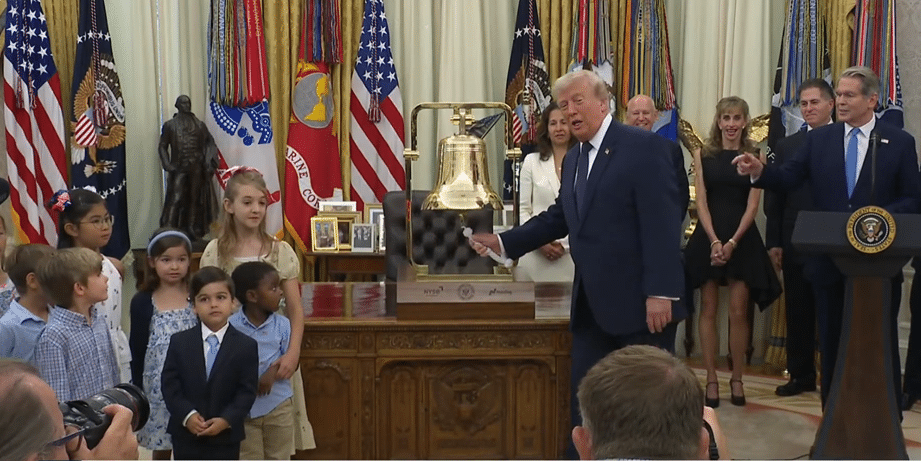

“They’re communists. They want to destroy our country. We’re not going to let that happen. But this helps even from the parents’ standpoint. You know, they see their child getting richer and richer as the … market goes up… If it goes up, they could become actually rich and their parents are going to be watching and we’re all going to be watching.”

That was President Donald Trump blasting communists as he rang the bell for the New York Stock Exchange and Nasdaq on July 6, blasting communists as he inaugurated in TrumpAccounts.gov that parents can now begin making contributions to, with more than 25 million accounts already created and plans to automatically enroll the rest of the 73 million Americans total under the age of 18. Funds invested go directly into an account indexed for the S&P 500.

In its history the S&P 500 has grown 9.8 percent a year on average, and so starting at $1,000 right now, if a child parents made monthly contributions of just $50 into the account, by the time the child was 18, it would be more than $35,000.

But that’s just the beginning. If the same person kept on making $50 monthly contributions — literally just $600 a year — by the time that person was 51, they’d be a millionaire. By the time he or she was 65, it would be $4 million. Totally doable.

Yes, there are risks as with any investment. There have been major market downturns in recent history, in 2000-2002 and again in 2008 and 2022. It happens, but with cost averaging, over time the average annual return has held true. Investors cannot predict when those downturns will occur, and with basic monthly contributions and cost averaging, they need not. Just keep making contributions and, with compounding growth, get rich.

Parents might even consider increasing contributions during downturns — not a bad way to reduce the cost basis of certain equities — and then when things do go up, there’s an even greater rate of return.

Really, it’s a bet on the U.S. economy, that American companies and everyone will continue to be prosperous, hard-working and that we will all become wealthier over time. It’s the reason companies and government offer pensions in the first place, not merely as an incentive, but an investment in the value of those employees.

With Trump accounts, we’re making an investment in the value of every child with defined contribution accounts. Instead of waiting to begin work to begin investing, parents can begin building that nest egg for their kids much earlier.

Fortunately, on their first day, the S&P 500 did happen to go up, by about 54 points, or 7,537.43, or 0.72 percent, but one day very soon it’ll go down for a day and maybe that’ll be a headline.

Now, say, there’s a downturn or we hit a bear market right now or soon. Naturally, the media and the President’s Democratic opponents in Congress will immediately wag their fingers and tell everyone what a terrible idea it was to buy the top of the market.

On average, year after year, they’ll end up being wrong. Or, you could be sitting around for months or years for a correction. Who knows what’s going to happen?

After decades and decades, we might be able to reliably look at the markets and say, you know, on average, they’re going to go up. Really, the argument will wind up being about when the best time to have begun investing really was. Just wait for a bottom, right?

No, the lesson is to get started as soon as possible. The future is now.

But it’s all par for the course. If President Trump is commander-in-chief and there’s a war, they hate Trump, so they have to root against the U.S. armed forces against Iran, even if it means Americans would die or Iran would get nuclear weapons if we did not act. The President is building a ball room but they hate Trump, and so they’ll think they need to tear it down later. He fixed the reflecting pool on the National Mall and so it must be vandalized. And so forth. It’s partisan sickness.

If there are Trump accounts, they hate Trump, and so they end up rooting for the economy to go down.

Ultimately, it’s an argument against ever investing. The reason for monthly contributions and cost averaging is exactly why professionals everywhere depend on 401ks and Individual Retirement Accounts (IRAs). It’s one of the major reasons why more and more Americans are able to become wealthy. The entire economy works on capital investment.

So, why would we discourage average Americans from investing and saving? But you watch, it’ll happen. And there’s a reason.

Do we really want to continue living in a country with economic disparities that in certain parts of the world have led to not merely economic destabilization, by political instability, and the rise of totalitarian parties?

Maybe that’s the point. Communists, socialists and fascists need depressions and disparities to rise to power. From their perspective, it makes sense. If we’re all successful then we all have something to lose if our constitutional and capitalist systems and our liberties are destroyed.

But America does not need any of that. Fortunately, there’s another way.

Instead, we can, as a nation, invest in our children’s futures, and there’s no need for any more socialist revolutions (there never was).

Trump accounts will ultimately be the best proof that a rising tide lifts all boats — and the next generation will see the value of the greatest economy — and the greatest country — in human history. And, as President Trump is fond of saying, the best is yet to come.

Robert Romano is the Executive Director of Americans for Limited Government.