By

By Late last week, House and Senate negotiators agreed to language for what is now a nearly $106 billion war supplemental, bringing to the floor of both bodies legislation that has been delayed for nearly 2 weeks.

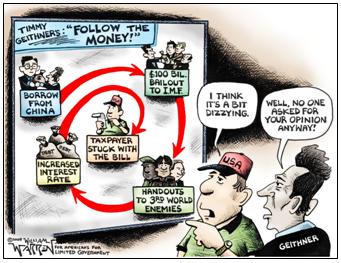

The trouble began when Republicans dropped their support for the supplemental on account of some $108 billion included for the International Monetary Fund. Unfortunately for taxpayers, the $100 billion credit line and $8 billion purchase of IMF Special Drawing Rights (SDR) were hidden in the bill. Appropriators agreed to only “count” it as some $5 billion in the spending bill, which is now on the fast track.

According to The Hill, House Democrats finally found the votes needed for passage of an ever-controversial war supplemental—from members of the House who have never supported the war efforts in Iraq and Afghanistan—because it included the IMF credit line: “Many of the 51 anti-war members who voted against the supplemental last month said they are willing to switch their vote because of the $5 billion for the IMF.”

Apparently, destroying the dollar is a greater priority than ending a war they purportedly hate. Although, according to Roll Call, Congressman John Murtha (D-PA) said Friday that “We don’t have the votes yet… Nancy’s working it right now. She’s trying to get the votes right this minute. I just heard her talking to a couple of Members. It’s going to be a very close vote.”

As usual, Barack Obama is demanding immediate action and predicting financial cataclysm should Congress not act. In his letter to Congress he wrote, “Many of the developing countries that would benefit from the [$550 billion expansion of IMF lines of credit worldwide] are experiencing severe economic decline and a massive withdrawal of capital. Should the situation become worse, and should the IMF not be in a position to stem the crisis, currencies could collapse. The experience with the Asian financial crisis shows that such a massive failure would be a catalyst for steeper drops in U.S. growth, jobs, and exports.”

In short, “Yippee, we have another crisis!”

By Obama’s own admission, the $100 billion credit is really just welfare for developing nations. What he doesn’t tell Congress or the American people is that the IMF credit extension actually helps China, Russia, and other foreign purchasers of U.S. treasuries to transition away from the dollar. And it will all be done rather simply.

Here’s how it works. The IMF is getting a huge boost from the international community of $500 billion, including the $100 billion from the U.S., taking its total assets to about $750 billion. With that, it can make loans and distribute aid to developing economies all around the world. The loans pay back interest to the IMF.

Now, in a new move, the IMF is selling bonds to nations, including China, Russia, India, and Brazil. According to Bloomberg News, these will “pay an interest rate pegged to the IMF’s basket of currencies, known as Special Drawing Rights.” China is buying as much as $50 billion, and Russia about $10 billion.

Russia is said to be “switch[ing] some of its reserves from U.S. Treasuries to International Monetary Fund bonds…” According to Alexei Ulyukayev, first deputy chairman of Russia’s central bank, reserves would be moved from treasuries into IMF debt. Those bonds will earn interest for the Russians, Chinese, and whoever else invests in them.

Which, of course, the U.S. is not. In the face of this blatant monetary aggression, the U.S. is borrowing money from these same creditors, and/or printing more cash, to “lend” it to the IMF to basically help them to make loans to allegedly needy nations and therefore leverage the sale of the bonds. What’s worse, if the IMF accepts treasuries as payment for the SDR-denominated bonds, a major run on dollar-backed assets could be seen.

In other words, U.S. taxpayers will be paying higher interest on the national debt in order to raise the cash necessary for the IMF to make loans, collect interest of their own, and then sell bonds—just like a central bank. In the process, the IMF’s Special Drawing Rights (SDR) become a de facto international reserve currency.

And in very short order, it will replace the dollar.

That is, unless the U.S. walks away from the table. And Congress keeps a shred of its dignity and refuses to honor Barack Obama’s $100 billion financial commitment he made at this April’s G20 summit. Americans for Limited Government recently published a background for journalists to explain the danger.

The $100 billion line of credit to the IMF would be the SDR equivalent of $100 billion on the date of the agreement. Currently the U.S. has a $10 billion line of credit to the IMF worth SDR 6.6 billion. The proposal would also increase the U.S. share in the IMF by SDR 4.97 billion at a cost of $8 billion, bringing the total commitment made by American taxpayers to $108 billion, greater than the war supplemental itself.

And members of Congress have the temerity to hide it by labeling it a mere $5 billion. Not all of the money will be drawn immediately, they argue. But as global economic conditions worsen or remain stagnant, and more nations turn to the IMF for loans and the SDR as a global reserve currency, that credit line will eventually be invoked.

All of which will leave American taxpayers with the bill, and gives the IMF the authority to dispense the cash however they wish—whether it goes to fund tin-pot third world dictatorships, or worse.

Of course, now the fix is in, and the most radical members of Congress have reportedly agreed to the $100 billion global bailout and dollar destruction plan. But look on the bright side. Perhaps when the dollar is completely worthless and interest payments on the now $11.3 trillion debt become unaffordable, and the nation is insolvent, Congress could always turn to the IMF for a loan.

Robert Romano is the Senior Editor of ALG News Bureau.