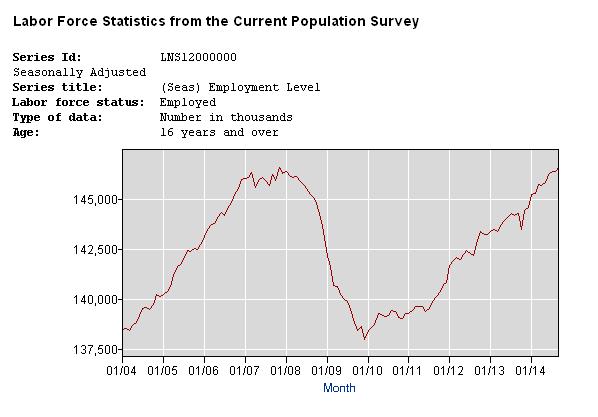

At the height of the Great Recession, by December 2009, 8.4 million jobs were lost. It has taken six years to recover to the 146.4 million January 2008 pre-downturn jobs level. Today, 146.6 million people have jobs, according to data compiled by the Bureau of Labor Statistics.

Here’s the problem. The population aged 16-64 has increased by 7.4 million since then.

It should be noted that the population over the age of 65 has also increased 8.4 million as people live longer and the Baby Boomers enter retirement. But that would skew the results here, so we’re leaving them out of the equation, and simply focusing on the7.4 million 16-64 year olds.

If the employment to population ratio for those aged 16-64 had remained where it was in, say, 2004 — then the percent who had jobs was 70.4 percent — 143.1 million of them would have jobs, instead of the current 138.6 million.

So, although the Obama administration likes to point out that the 8 million jobs lost have finally been recovered, once population growth is taken into account, it turns out we’re still 4.4 million jobs short of a true recovery.

The reason for the slack is that since the labor market hit its December 2009 bottom, it has only been averaging a little less than 151,000 new jobs a month. To have fostered a real recovery, the economy really needed to have produced 225,000 new jobs a month during that time.

If we had created the jobs we needed, there would’ve been greater competition for labor, resulting in higher wages. Instead, incomes are flat and the recovery has been quite sluggish.

Here’s the good news. Remember that the 16-64 aged population grew by 7.4 million since the downturn began? Well, 6.9 million of them are aged 55-64. It turns out the population 16-54 only grew by about 500,000.

Within 5-10 years, those 55-64 year olds will be entering retirement age as well. By then, the problem might be there are not enough people to fill all of the jobs.

But then we’ll have an entirely different problem: The top-heavy entitlement state with all of the seniors in the Social Security and Medicare system. The federal budget will be busting at the seams, and pressure will be increasing on a comparatively smaller workforce to pay more in payroll taxes, particularly should interest rates rise. Why?

Because if they do, borrowing costs for the federal government will be rising, meaning less money can be raised via treasuries sales. Yet, here’s the rub, the government is also once again expecting trillion dollar a year deficits by the end of this decade, so the money’s got to come from somewhere.

The choice for millennials will be to either borrow the nation into oblivion, or tax it into the Abyss. But those lead first to an out-of-control welfare state and, later, to financial ruin.

Meaning the only real option is to reform the ship of state before it sinks.

Either way, a jobs boom by the end of this decade will be more than welcome to assist the lagging recovery.

However, the only solution to our longer term challenges, truth be told, is robust economic and population growth. Americans need to start having more kids, establishing new businesses, and creating new jobs.

But we won’t get there if the cost of living and doing business is rising dramatically because of government policies, and short-sighted fiscal considerations.

If a relatively smaller workforce is going to pay for all these seniors entering retirement, there are going to have to be major cuts elsewhere in the budget, and there is going to have to be a major prosperity incentive to grow the economy and raise families.

Robert Romano is the senior editor of Americans for Limited Government.