A piece on currency manipulation by this author, “China and the world’s trade war against the U.S. — and why we’re losing” apparently warranted a response from the popular economics blog, Cafe Hayek, “An Open Letter to Robert Romano,” by George Mason University Economics Professor Donald Boudreaux.

It is quite an honor, actually. Professor Boudreaux is world-renowned in his field, and usually one has to be a particular New York Times columnist and fellow economist to garner such a reply. (See: “An Open Letter to Paul Krugman” and “Yet Another Open Letter to Paul Krugman.”)

In his response, Professor Boudreaux makes some rather interesting contentions, including that the premise that “Beijing has long kept the prices of Chinese exports artificially low by keeping the value of the Chinese yuan artificially low” is “contrary to fact”.

While we thank Professor Boudreaux and the Mercatus Center for taking such an interest in my column, we stand by its initial premise. In fact, China pegs the yuan below the dollar and has accumulated a horde of U.S. dollar-denominated assets including treasuries, mortgage-backed securities, corporate debt and equities, now at almost $1.7 trillion, and specifically, this has had the effect of reducing the cost of Chinese exports in the U.S.

First, that China pegs the yuan below the dollar and has for years, as is their sovereign right to do so, is essentially common knowledge. We very much doubt this is in dispute. One can easily research the value of the yuan’s fixed exchange rate on the Bank of China’s website. It is absolutely artificial. Floating exchange rates are artificial, too, for what it’s worth. So is money.

As for the dollar-yuan exchange rates, since 1994, 1 dollar has equaled on a fixed basis as many as 8.62 yuan, or about 6 yuan in 2014. But fixed and cheaper than the dollar it has remained according to the desires of policymakers in Beijing.

To the second point, this particular exchange rate policy certainly has acted to make Chinese exports to the U.S. cheaper than they otherwise would be. How this works in theory is, say, the dollar and yuan have a 1 to 1 exchange rate, and widgets sell for $4 in the U.S., whether produced domestically or imported from China. But then China says, no, the exchange rate is now 1 dollar equals 3 yuan. Suddenly the price of Chinese widgets in principle drops to $1.33 in the U.S., while the U.S. widget still costs $4. Meanwhile, in China, the cost of U.S. made widgets jumps to 12 yuan while the Chinese made widgets remain 4 yuan there.

Again, one need not look far for literature on the topic since in practice, it works very similarly. An Oct. 2015 World Economic Outlook from the International Monetary Fund (IMF) study of 60 economies including China found that “A depreciation in an economy’s currency is typically associated with lower export prices paid by foreigners and higher domestic import prices, and these price changes, in turn, lead to a rise in exports and a decline in imports. Reflecting these channels, a 10 percent real effective exchange rate depreciation implies, on average, a 1.5 percent of GDP increase in real net exports,” which much of the increase happening in the first year.

This means that the more exporters have devalued their currencies in recent history — whether through fixed exchange rates or building up foreign exchange reserves or both — the more products they were able to export.

The IMF is not alone in this regard, with economists from the left such as Paul Krugman and on the right like Art Laffer who have agreed that currency manipulation matters to trade and jobs — a lot.

Writing for Forbes in a 2015 oped, “Currency manipulation and its impact on free trade,” Laffer states, “currency manipulation is a potent tool of mercantilists, tempting nations to increase their trade balances and export domestic unemployment to the countries that are not devaluing, a ‘beggar-thy-neighbor’ approach to international economics.”

Laffer cites a Peterson Institute for International Economics study of 20 nations that found “the currencies of the interveners [that are] substantially undervalued [boost] their international competitiveness and trade surpluses,” costing anywhere from 1 to 5 million jobs in the U.S. and contributing $200 billion to $500 billion to our annual trade deficits.

As for Krugman, although he no longer believes the yuan is undervalued in its current iteration, his views on the impact of China’s devaluation in the 2000s is clear. In 2010, he wrote, “This is the most distortionary exchange rate policy any major nation has ever followed. And it’s a policy that seriously damages the rest of the world. Most of the world’s large economies are stuck in a liquidity trap — deeply depressed, but unable to generate a recovery by cutting interest rates because the relevant rates are already near zero. China, by engineering an unwarranted trade surplus, is in effect imposing an anti-stimulus on these economies, which they can’t offset.”

Certainly the extent to which currency devaluation competitively reduces the prices of exports of the nation that engages in the depreciation, if any, is a highly debated topic in economics. Either they do or they don’t, and policymakers will or will not respond accordingly.

We say they do, and that the policy is a conscious choice by exporting nations like China to achieve just that outcome. Just as doing almost nothing in response has similarly been a choice by U.S. policymakers for years.

Now, one can argue that the cheaper goods are actually to our benefit, since we save money on the prices of those goods. After all, who doesn’t like cheaper goods? But with this benefit has come several other costs, all outlined in the original piece.

The resulting trade deficits helped fuel the emerging markets bubble and emerging markets’ need for oil and industrialization, which blew up the price of commodities throughout the 2000s across the board. Also, as the trade deficits were reinvested in the U.S. dollar-denominated assets including U.S. treasuries, mortgage-backed securities, corporate bonds and equities, it helped blow up the U.S. housing and stock bubbles in the 2000s and helped drive interest rates down. Those bubbles helped facilitate the borrowing binge in the U.S. that led directly to the financial crisis of 2007 and 2008. Other costs include fewer jobs particularly in manufacturing, lower labor participation, flattening incomes, higher fiscal budget deficits, more debt, reduced U.S. market share in manufacturing globally and slower economic growth.

The blame, correctly assigned, would not be on China per se, which is acting in its own perceived national interest, but on U.S. policy makers that failed to do anything meaningful in response, and particularly on Congress, which granted permanent normal trade relations with China in 2000 without ever addressing the fundamental issue of the yuan’s fixed exchange rate or Beijing’s accumulation of foreign exchange reserves.

Finally, we never contended that “Beijing really is ensuring that Americans continue to buy Chinese-made goods at prices below the Chinese’s costs of producing these goods,” as Boudreaux claimed, since our actual argument is that Chinese companies have profited from the current arrangement.

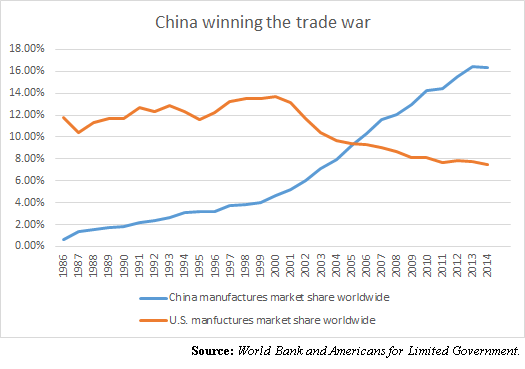

While Chinese companies’ profit margins were likely smaller per unit sold than they otherwise might have been without the devaluation, China has more than made up for it through sheer volume. They still made money. This has led to a massive increase in China’s global manufactures market share, from 4.67 percent in 2000 to 16.35 percent in 2014, according to data compiled by the World Bank on worldwide exported manufactures as a percent of exports worldwide. That cannot be accomplished without being profitable.

The U.S. on the other hand, has lost global market share in that same time frame, from 13.74 percent to 7.45 percent in 2014, as manufacturers have shifted operations overseas.

Which was the point of the original piece, that we’re in a trade war, which the U.S. is losing. Professor Boudreaux says there is no war and that even if there was China’s waging it against its own citizens. But then again, he cannot see how exchange rates or stockpiling foreign exchange reserves might even impact on trade or prices, so sees no case for addressing what he views to be a non-problem.

If that is the attitude that pervades with policymakers in Washington, D.C., perhaps that explains why in this war, China is winning, and we’re not even fighting.

Robert Romano is the senior editor of Americans for Limited Government.