In 2016, when President Donald Trump ran on his America first trade agenda, much of the conventional wisdom was that, if implemented, his tariffs would wreck the U.S. economy. It would have the same impact as the 1930 Smoot-Hawley Act, and so the prediction goes, lead to another Great Depression.

“Trump trade plans could cause global recession: Experts,” read one confident headline on CNBC in May 2016.

“If you take (Trump’s) position as real, that we would do this, then it would take the world down the road that we saw in the 1930s that we saw with the Smoot–Hawley Tariff,” Caroline Freund of the Peterson Institute for International Economics said. “The world would definitely fall into a recession.”

The Washington Post’s Robert Samuelson wrote in June 2018, “The ghost of Smoot-Hawley seems to haunt Trump,” after Trump levied tariffs on steel and aluminum.

Samuelson suggested, “What’s eerie is that Trump’s embrace of protectionism is now assuming the same role as Smoot-Hawley in the 1930s. By slowing economic growth, it darkens the outlook and reduces the ability of debtors to repay their lenders. So much for the lessons of history.”

Other predictions have suggested, besides slowing economic growth or perhaps a global recession (and presumably much higher unemployment), there would be consumer inflation as the taxes raised prices on goods.

So, how has it all played out? President Trump began levying tariffs on steel and aluminum in 2018, and in the second half of last year, hit China with a 25 percent tariff on $50 billion of high-tech goods and another 10 percent on $200 billion of goods and then raised it this month on the latter to 25 percent.

So far, at least, the predictions of doom have not come to pass.

Growth in 2018 came in at 2.9 percent, the best since 2015, and the first quarter of 2019 surprised at 3.2 percent in spite of predictions that the partial government shutdown would hurt the economy.

Unemployment is at a 49-year low at 3.6 percent.

Inflation is stable at 2.0 percent the past 12 months.

So far, so good.

But all of that is in the rear-view mirror, and so the question going forward is whether it will last. Surely, if the economy turns south, Trump’ critics will lay into the tariffs and say they are the cause of any slowdown that might happen now.

But what if the economy doesn’t tank? What if, despite the tariffs, we continue to see good growth, steady job creation and price stability? Will Trump’s critics figure out that tariffs, on their own, do not cause economic slowdowns?

There are many differences between the U.S. economy today and the one in 1929 that entered the Great Depression obviously. Back then, we were a net exporter, today we are net importer. By employing tariffs, when the U.S. was already the source for many of the goods the global economy was buying, no new market share was gained. Instead, it provoked retaliatory tariffs that hurt America’s dominant market position at the time.

Arguably, China today is in a more comparable position to the U.S. in 1929, being a global manufacturing powerhouse that has rapidly expanded its global market share the past 20 years.

Another factor to consider is that just as suddenly as trade talks with China have broken down, they could resume in short order and head off a retaliatory cycle.

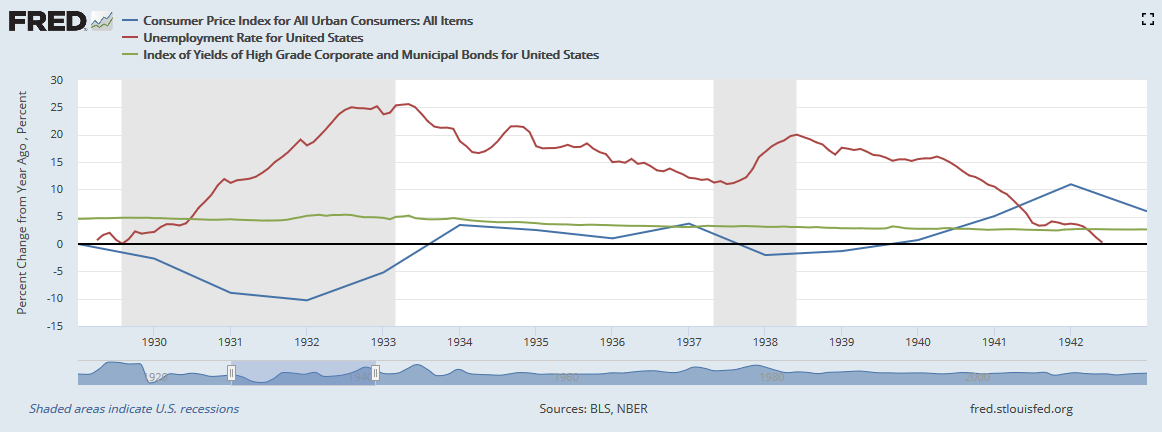

It is also worth noting that the market crash and bank runs began in 1929. Deflation began as early as 1927, slowed in 1929, and then went crazy starting in 1930. Nominal interest rates did not adjust enough, resulting in a real interest rate that was rising at the same time debts could not be repaid. By 1931, the bank failures went global and the interwar gold standard fell in short order by 1933.

By that time credit outstanding had risen to close to 300 percent of the Gross Domestic Product, as noted by Hoisington Investment Management Economist and Executive Vice President Dr. Lacy Hunt.

The Smoot-Hawley tariffs did not take effect until 1930. It is impossible to know how the economy would have proceeded without the tariffs — the conventional wisdom was they exacerbated the Depression — but deflation and the consequential unemployment it wrought might have been a problem with or without them.

We cannot know the counterfactual, but we can say is that today, we’re not in a deflationary cycle, inflation is stable and unemployment is quite low.

The Great Depression was a catastrophic sea change in the global monetary system that had followed a period of rapid credit expansion. So, just because tariffs were enacted does not mean they were the root cause for the contraction. With prices falling so much, global trade could have ground to a halt all the same.

The fact is, all these things were happening at the same time. The tariffs went into effect in March 1930. Deflation began dramatically ensuing in July 1930 as did unemployment. But correlation is not always causation. Were tariffs truly the cause of the rise in unemployment in the 1930s? A strong case can be made that it was the deflation.

We’re already a year into the Trump tariffs. If we were going to see a Great Depression with catastrophic deflation and unemployment in a vicious cycle, shouldn’t we be seeing it by now? If not now, when?

Finally, even if we do have another recession sometime soon, who’s to say we are not simply nearing the nearing the end of the business cycle? No boom lasts forever. Eventually there will be a correction.

What separated the Great Depression from other recessions was that unemployment remained elevated even after the economy started growing again all the way until World War II. Maybe I’ll eat my words, but on that latter point I am skeptical history will repeat itself with catastrophic unemployment the next time we do get a recession. We’ll see. Stay tuned.

Robert Romano is the Vice President of Public Policy at Americans for Limited Government.