The U.S. economy contracted by a massive, inflation-adjusted 4.8 percent in the first quarter according to the Bureau of Economic Analysis as job losses topped 30.3 million with another 3.8 million initial unemployment insurance claims in the federal and state governments’ bids to stop the Chinese coronavirus pandemic.

Factor in the 5.8 million who already were unemployed when unemployment was at a 50-year low of 3.5 percent, and the effective unemployment rate could already be 21.9 percent with 36 million out of work.

All that in just six weeks. Something to keep in mind the next time the government wants to encourage people not to work with Green New Deal or universal income schemes, the damage of which would be equally devastating.

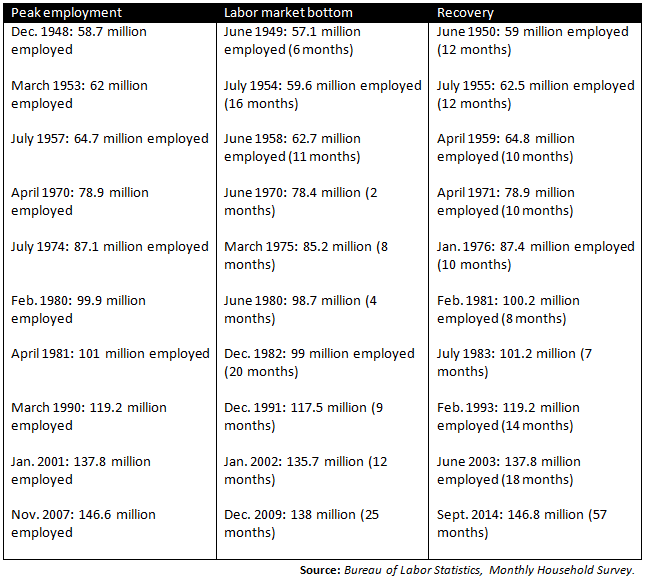

In comparison, it took two-and-a-half years to get to 25 percent unemployment in the 1930s as deflation washed away the global economy, four years to get back down to 11 percent, and then not was not until the U.S. entry into World War II that the numbers got back to “full” employment with millions of men enlisted in the armed forces.

More than a decade ago in the Great Recession and the financial crisis, it took more than two years to lose 8.3 million jobs, and then almost five years to get those jobs back.

Unknown factors that might make that number slightly lower are small businesses who have applied for payroll protection since the economic crisis brought on by the state government-directed closures began.

On the other hand, the number could also be much larger when overwhelmed state unemployment claims systems and off-the-books employers letting workers go who would have been ineligible for unemployment insurance are all taken into account.

We’ll have some more information to consider when the Bureau of Labor Statistics releases the monthly unemployment report on May 8 and when we get to see how many people remained on unemployment assistance through April with continued claims.

Making matters worse, if past recessions and interest rates are any guide, the economic devastation could continue to mount even after states are fully reopened as the cycle works its way through.

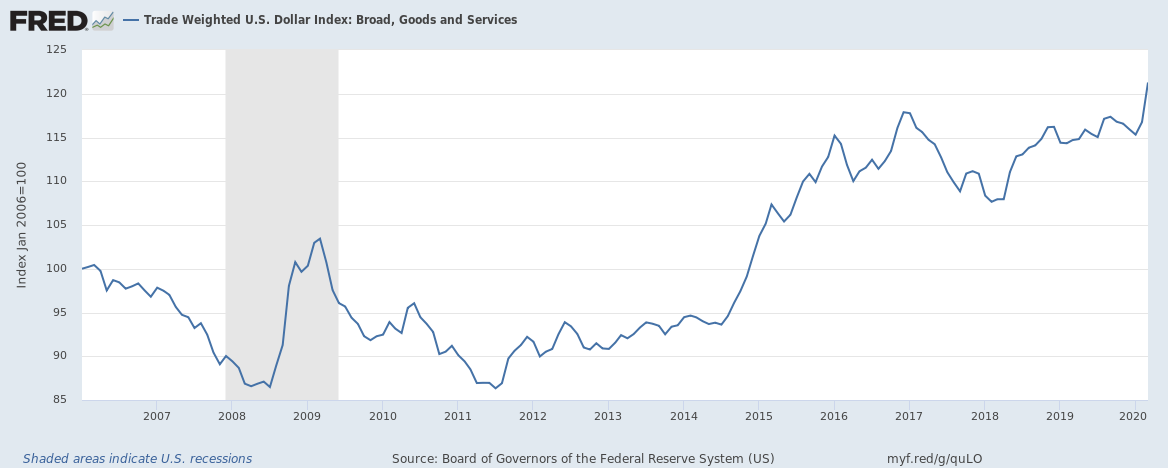

Should deflation set in with the U.S. dollar stronger than ever relative to that of foreign trade partners as central banks and financial institutions flood into U.S. treasuries and other dollar-denominated assets in a flight to safety, that could make things even worse.

You see, the economy is actually quite a delicate thing. It cannot be turned on and off like a light switch. It took about a month to get it on the ground to slow the spread of COVID-19 and save as many lives as possible. Now, as the virus wanes, how long it will take to get it back up in the air is anyone’s guess.

As the bad economic news continues to mount, all eyes turn towards President Donald Trump, Congress and phase four legislation intent on jumpstarting the U.S. economy. If there was ever a time both parties need to work together, it is right now. Failure to act in a timely manner could jeopardize society itself.

Already the federal government has responded with more than $2.7 trillion that can be leveraged up to more than $6 trillion to save small and large businesses and to prop corporate and municipal bond markets.

In terms of how large phase four will need to be, I’d say think big, Mr. President. It will extraordinary leadership to lead us out of the virus-induced depression we suddenly find ourselves in, and so far, as the job losses mount by the millions on a weekly basis, no matter how big we think the problem is — it is probably much, much bigger.

Robert Romano is the Vice President of Public Policy at Americans for Limited Government.

{kind=link}