A picture is worth a thousand words.

“Walmart: Now hiring, $17 per hour.”

No, that is not Photoshopped. It is an actual help wanted sign from Williston, N.D. The story is the shale oil boom taking place there that has resulted in an explosion of demand for labor, a surge in property values, and a bevy of new construction.

In fact, North Dakota leads the nation in the growth of home values at 8.3 percent year over year as of September according to Freddie Mac. And it is also the envy of the post-financial crisis economy with the lowest unemployment rate anywhere at 2.8 percent in October, according to data compiled by the Bureau of Labor Statistics.

The simple reason is growth. North Dakota went from a field production monthly total of 2.6 million barrels of oil in September 2004 to almost 36 million barrels in September 2014 thanks to shale oil fracking.

There was no hike in the minimum wage there — it remains $7.25 an hour. No onslaught of wage and hour regulations. No redistribution of wealth or stupid tax credits or welfare. Just innovation and growth that has created over 136,000 jobs — a 40 percent increase — in the past decade in an area so sparsely population it barely registers on the electoral college.

To put those 136,000 jobs into perspective, it outpaced the growth of population in the state. That is to say, everyone who moved to North Dakota or came of age there has pretty much found a job.

There is such a shortage of labor there that, yes, to fill certain shifts Walmart is willing to pay people $17 an hour.

Now, with oil prices crashing in the past many months on weakening demand globally, one might expect a slowdown in production, a cooling of home values if not a drop, and a slowdown in wages. Perhaps a temporary increase in unemployment.

But the point stands. Legitimate growth in production over several years created a surplus demand for labor, a surge in wages, and a boom for housing.

Contrast all of that with the aptly-titled yet wildly off-the-mark editorial from the New York Times, “Homeownership and wealth creation.”

The housing bubble was unsustainable, but, writes the editorial board, “the lesson of that debacle is not for individuals to avoid home ownership or for policy makers to devalue its importance. Rather, the lesson should be to foster conditions under which middle-and lower-income Americans can sustain homeownership and avoid the ruin of foreclosure.”

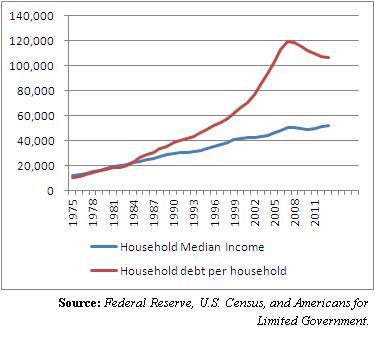

The Times concludes, “The solution is to lift wages.” There’s certainly an element of truth here. Household debt has outpaced household median income for almost 40 years.

From 1976-2006, right before the bubble popped, home values accelerated at an average 6.17 percent a year, according to the Freddie Mac Home Price Index.

Comparatively, median income only grew at a 4.61 percent average nominal rate during those years.

The result? Household debt per household grew at a whopping 8.11 percent a year, according to data by the U.S. Census and the Federal Reserve. In 1975, the debt to income ratio was just 90.1 percent. By 2007, it had grown to 237 percent. The rest is history.

Debt remains far too high, and income far too low, for far too many Americans. That explains how we got here, certainly. So, lift wages, by all means. But how to address these structural imbalances?

Not growth, says the Times, but “new policies like higher minimum wages and toughened labor standards, [and] also with approaches to managing the economy to ensure that a fair share of growth goes to wages and salaries, rather than going disproportionately to corporate profits.” This, the board advises, will increase incomes and thus raise home ownership and wealth.

Similarly, the White House proposes raising the minimum wage to $10.10, and in February plans to issue a new rule to increase the $23,000 minimum amount an employee needs to make before his employer can exempt him from federal overtime rules. The Center for American Progress wants the threshold increased to $50,000.

Which, they are welcome to try. Good luck with that. But the administration and Times editorial board should be forewarned that these policies are not likely to lead to any substantial increases in production. They won’t lead to greater demand for labor or for housing.

Nor will they appreciably increase home values or lift wages for the vast majority of Americans who are stuck in the same slow economy as everyone else.

That is, not the way growth could. The truth is, when there is real growth more than a “fair share of growth goes to wages and salaries,” as evidenced in North Dakota.

If the U.S. wants to get out of its economic straitjacket, and truly lift wages, the solution is to create incentives to increase production across every sector of the economy. To make things here and innovate once again.

The real solution is not for government to divide up a shrinking pie, but for it to get out of the way so the pie can grow once again.

Robert Romano is the senior editor of Americans for Limited Government.