The U.S. economy created over 3.8 million jobs in May in the Bureau of Labor Statistics’ household survey, and 2.5 million in its establishment survey, heralding the bottom of labor markets in April.

How do we know April was the bottom? Unless we’re anticipating losing 3.8 million jobs in June when America is reopening, barring a resurgence of the COVID-19 pandemic, when the momentum is moving precisely in the opposite direction, the likelihood is that June, July and August will only add to what has already been gained.

That will mean boosted labor participation, which added 1.7 million Americans back to the civilian labor force last month alone.

And a lower overall unemployment rate.

So, millions of jobs added each month, reaching a fever pitch this summer in time for the political conventions, highlighting easing concerns over the COVID-19 pandemic and the current protests and riots, and it’s easy to see how President Donald Trump and his reelection bid will be dramatically strengthened.

It’s not hard to predict at all.

Americans for Limited Government President Rick Manning praised the numbers, stating that the “employment numbers confirm that we’ve turned the corner on the Chinese originated virus economic disaster. More people are working, more people are in the workforce, and America is reopening. This is great news for the millions of Americans who fear that they may not have a job to return to. It is also a confirmation of President Trump’s emphasis on supporting small and mid-sized businesses that were either shut down or damaged as a result of the Covid-19 response.”

So far, the sectors of the economy benefitting the most from reopening include: 391,000 added in health care, 464,000 in construction, 225,000 in manufacturing, and 367,000 in retail.

Other factors lending to the current upside include the now weakening dollar from its record highs during the height of the pandemic, making deflation less likely during the recession, at least for now. A sudden strengthening of the dollar might reverse those gains.

Oil appears to be resurgent after OPEC agreed to production cuts into July but remains very volatile.

Add to the picture that Americans have been cooped up for months on end, and one can see a big recipe for pent-up demand fueling a recovery this summer. The question is how rapid it will be.

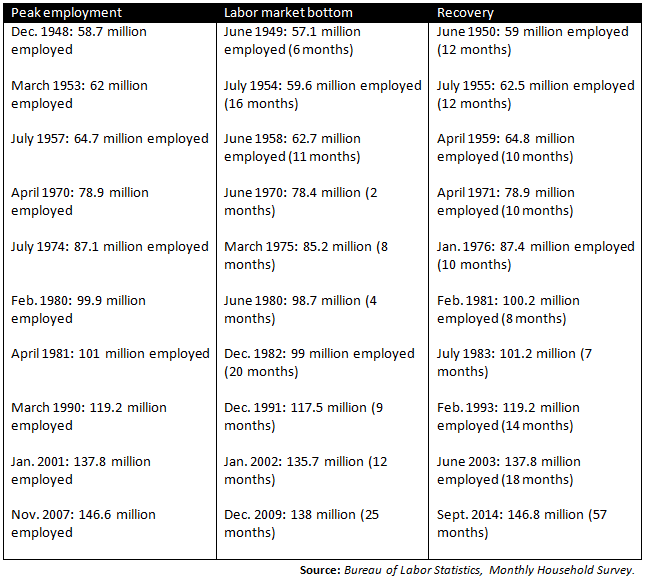

The good news is that with the labor market bottom having already been felt in April, this recession has already beat the financial crisis and Great Recession, when it took 25 months for all the jobs to be lost, and about five years to recover. Here, it took just two months for the worst of the job losses to be felt.

So if the downswing was that rapid, then it’s easier to make a case that so too will be the upside. However, should the job gains slow down considerably next month, that would be a large cause for concern.

Assuming the charts continue to be pointed in the right direction, very soon, President Trump can claim some vindication of his June 3 prediction that “I feel more and more confident that our economy is in the early stages of coming back very strong. Not everyone agrees with me, but I have little doubt. Watch for September, October, November. Next year will be one of the best ever, and look at the Stock Market NOW!”

So far, the way things are playing out, Trump may be right and it may even be on an accelerated timetable, months sooner than expected. In the political back and forth then between President Trump and former Vice President Joe Biden, then, so far it seems to be the advantage is yielding to Trump.

Robert Romano is the Vice President of Public Policy at Americans for Limited Government.

{kind=link}